Thursday, February 24, 2011

Variable vs Fixed Mortgages

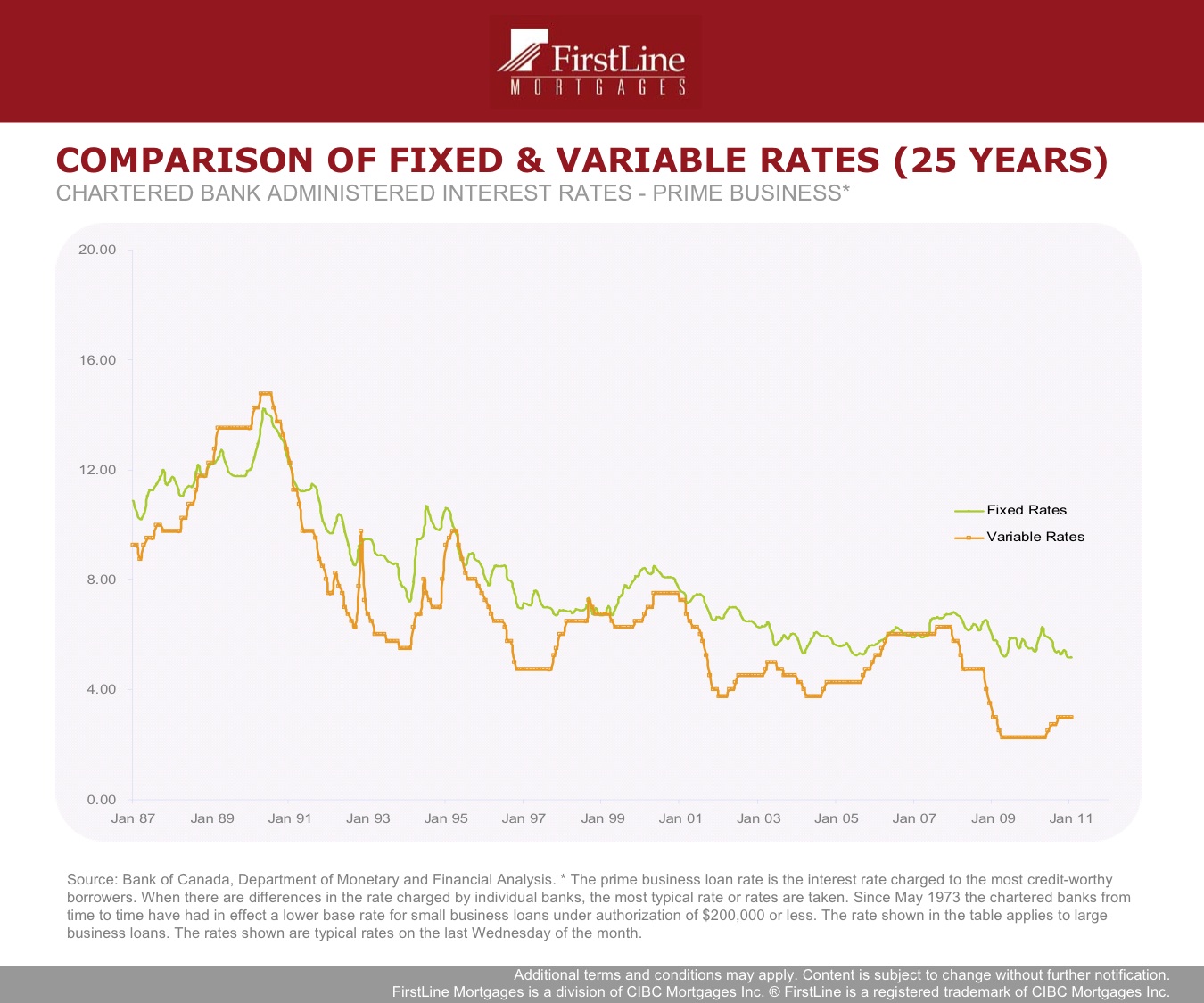

Here is a graph from Firstline Mortgages showing the comparison between fixed and variable mortgage rates over the past 25 years - Historically variable has been the way to go.

Saturday, February 12, 2011

My article in the New Condo Guide. Feb4 - Mar4, 2011

New rules to address a long-term problem.

Finance Minister Jim Flaherty introduced new changes to mortgage rules to address a long-term problem -- Canadians carrying an historically large amount of debt. The recent financial crisis may have brought more attention to this growing problem, and this is the government’s way of trying to avoid anything like what we have seen in the United States.

Mortgages are one of the largest household expenses and one of the few areas the government can still impact consumer spending. The government attributes a lot of the growing problem to high-risk mortgages, credit card debt, longer mortgage amortizations and the Home Secured Line of Credit (HELOC).

The new changes are aimed chiefly at these issues:

• The amortization period is reduced to 30 years from 35 years

• The loan to value available for refinancing your home is 85%

• Secured lines of credit will no longer be insured, maximum loan to value will now be 80%.

This would not be the first time the government has taken action in the mortgage market. In 2008, the Government reduced 40-year amortizations to 35 years, eliminated the 100% financing and the interest only mortgages. So the Finance Ministry is slowly repealing some of the more ‘lenient’ lending practices from a few years ago.

Two of the three changes address the concern the government has with Canadians taking on too much debt, that being, the changes to refinances and HELOCs. Essentially, those are the two methods that some Canadians use to take on large amounts of 'Bad' debt, debt that is used to purchase depreciating assets or consumer goods versus 'Good' debt, debt used to purchase investments, start a business or buy appreciating assets like real estate.

Regarding the reduction in amortization to 30 years, it affects the homebuyer, but only marginally. Payments are approximately $100 more per month on a 30-year amortization versus a 35-year based on $300,000 mortgage at today’s rates.

Although these changes may restrict the number of individuals that qualify for a mortgage, it may provide the incentive to those considering a home purchase to act. Three compelling reasons to purchase sooner, rather than later:

• Recent correction in Home prices

• Interest rates are still at historic lows

• Pending mortgage rule changes

Tuesday, February 1, 2011

Edmonton Reno Show

My colleague Stacey Petruch and I will be participating in this year's Reno Show. Feb. 4-6, 2011

We will have information on:

We will have information on:

- Ways to make your home more energy-efficient

- Hiring a Contractor

- Tips on renovating your Windows/Doors

- Tips on renovating your Bathroom

- Tips on renovating your Kitchen

And obviously, we'll be there to answer your questions on how to pay for it all. Stop by our booth, say hello and enter our draw to win a new iPad.

Subscribe to:

Posts (Atom)